The Goals feature allows users to set various financial goals within Vision Money, such as home purchase, children’s education, retirement, and other expenses. It calculates the future cash flow to achieve these goals, integrates with the accounting function to monitor goal progress, and analyzes factors such as income, expenses, and investment returns. It also calculates the insurance coverage needed for family responsibilities through the discount value of financial goal setting.

List of Goals Features

Main Menu->My Goals

Users can set financial goals within Vision Money, including budget and investment return. The features include:

- Set the priority of goals.

- Specify whether a goal belongs to personal consumption or family responsibility. In the event of the individual’s life termination, determine if the financial goal still needs to be achieved, which falls under family responsibility.

- Calculate the future monthly asset balance.

- Calculate the minimum investment return(IRR) needed to achieve all goals (future monthly asset balance equal or greater than zero).

- Target assets to achieve goals (Discount value of future goals; Discount rate is target Return)

- Current assets to achieve goals (Discount value of future goals; Discount rate is target Return)

- Need life insurance coverage(Discount value of family responsibilities goals; Discount rate is target Return)

- Monthly target net asset calculation formula: Beginning of the month target net asset+Monthly income goal−Monthly expense goal+ Investment return=End of the month target net asset

- Investment return= (Beginning of the month asset balance+Monthly income goal−Monthly expense goal)×Monthly return

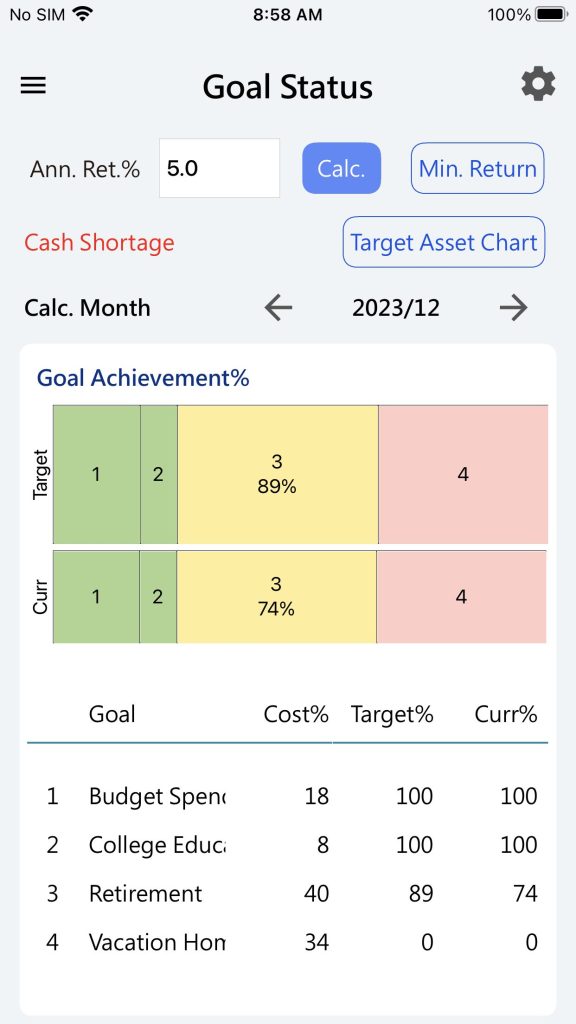

Feasibility of goal completion

- Prioritize goals and automatically list the current monthly budget as the top priority. Green blocks indicate goals that can be fully achieved, yellow blocks represent partially achievable goals, and red blocks signify goals that cannot be achieved at all. Achieve asset-related financial goals sequentially based on priority.

- Set various financial goals, and it’s not necessary to complete them all at once in the plan. For example, you can set a goal to travel around the world, and it can be prioritized last. This goal will only be completed after the goals with higher priority are achieved.

- Cost%: Future financial goals are assessed based on the sum of discounted cash flows, revealing the proportion of assets required for this goal compared to others.

- Ann. Ret%: The investment annual return. Press “Calculate” to compute various values such as period-end asset balances, asset achievement rates, goal feasibility, and required coverage amount based on this investment annual return. Changes in the annual return will only affect the target asset-related values and will not impact the actual assets or investment conditions.

- Min. Return: Calculates the minimum annual investment return(IRR) required to achieve all goals.

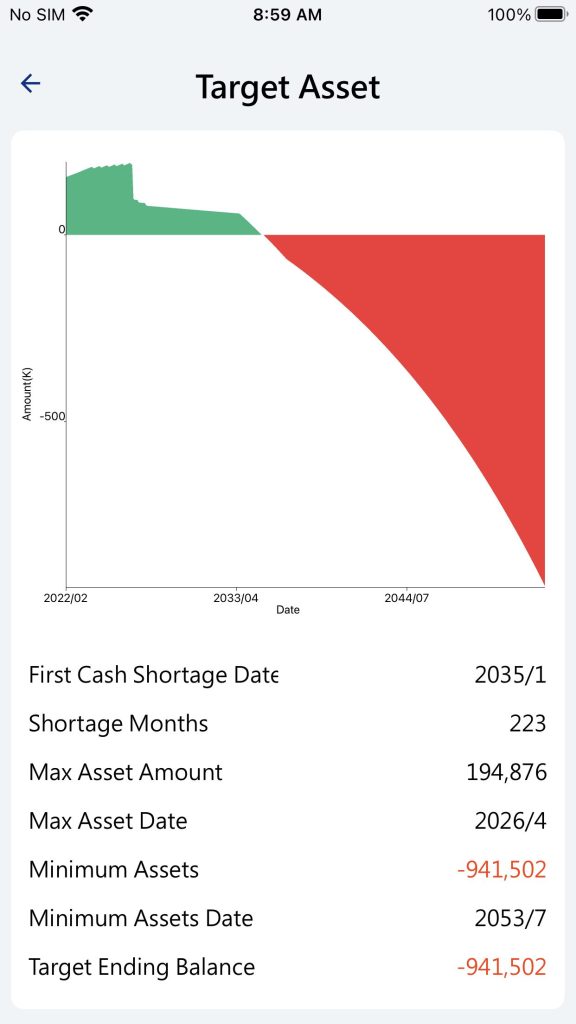

- Cash Shortage, Unable to Achieve Goals / Cash Surplus, Goals Attainable: If the target assets for any future month are negative, it will display “Cash Shortage, Unable to Achieve Goals.” If the target assets for all future months are non-negative, it will display “Cash Surplus, Goals Attainable.

- Target Asset Chart: Please refer to Target Asset Chart

- Calc. Month: Use the left and right arrows to change the calculation month and year. The values below are calculated based on the end of this selected month.

- Target%: The percentage of the goal completion is projected based on the asset balance for the initial date.

- Current%: The anticipated percentage of goal completion is based on the current asset balance.

- The target assets exceed the current assets, resulting in a higher percentage of anticipated goal completion compared to the current achievable percentage.

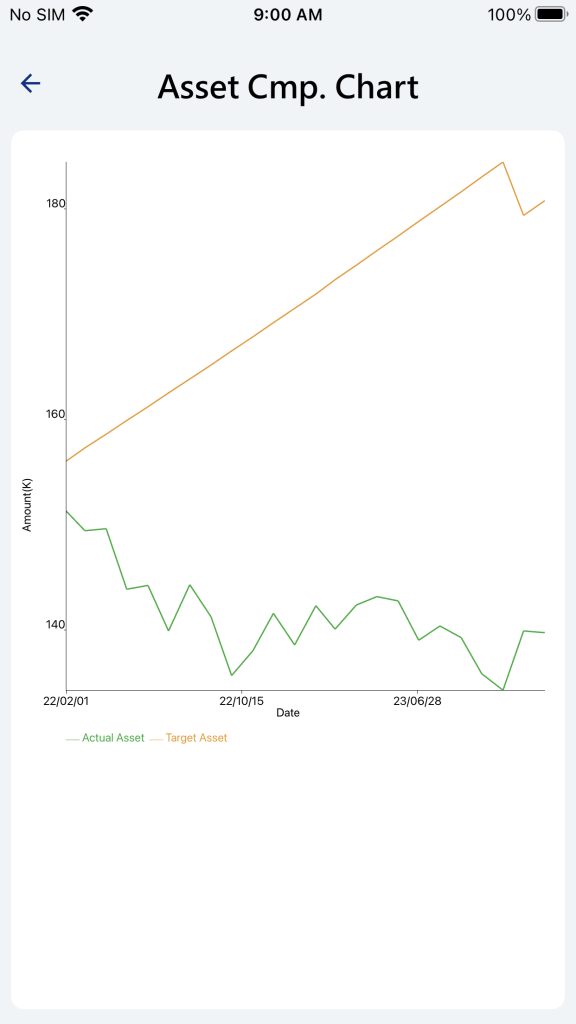

Target Assets Chart

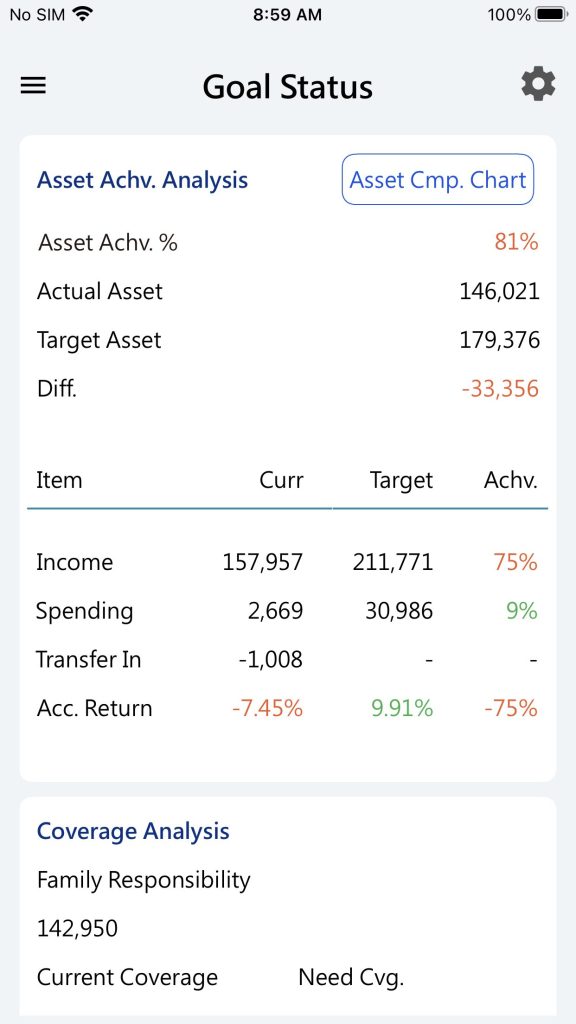

Goal achievement status

- Asset Comp. Chart: Compare Actual Assets and Target Assets in the period.

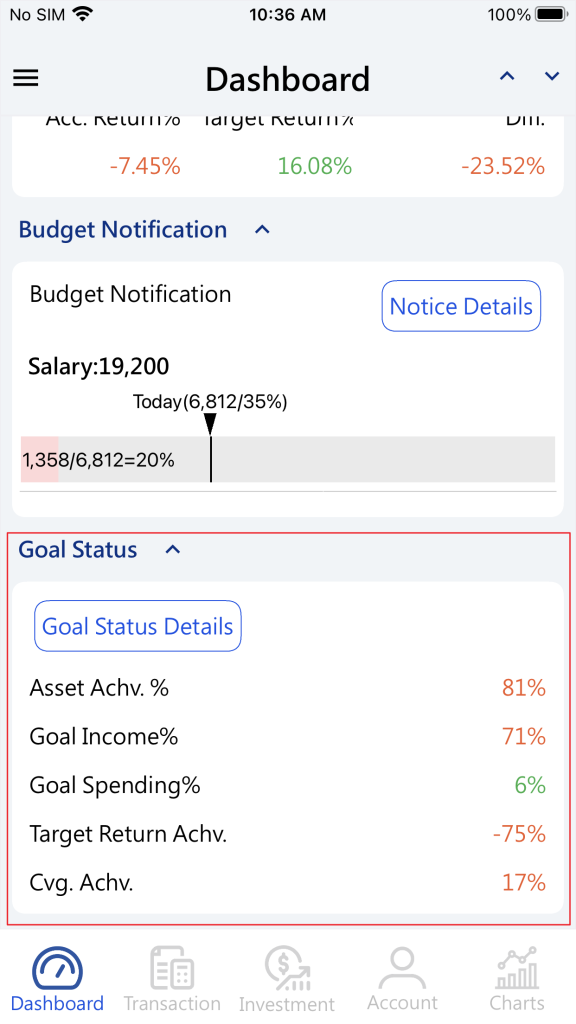

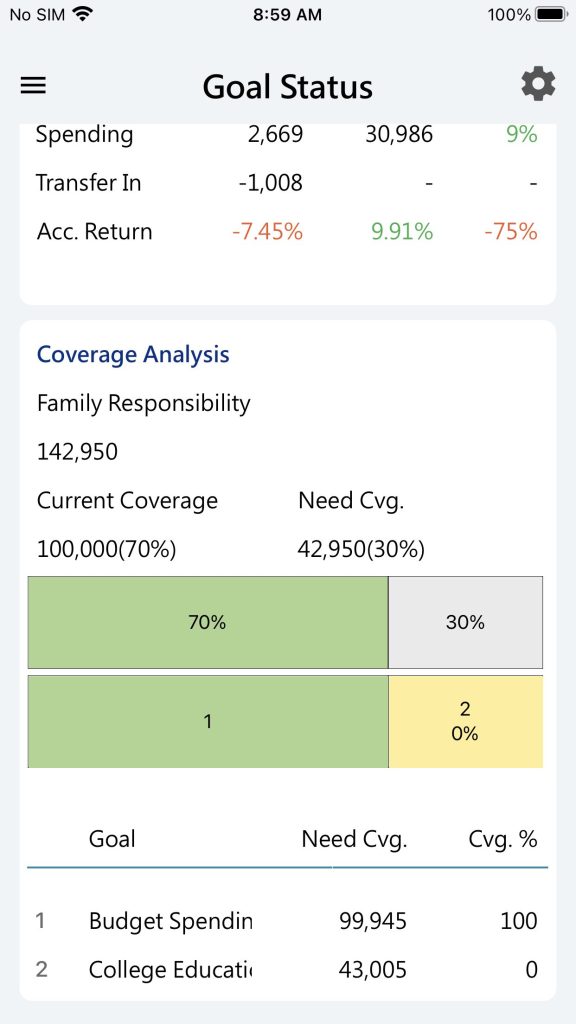

- Asset Achievement Rate: Current Net Assets / Target Net Assets

- Actual Net Assets: The net value of accounts included in the plan as of the selected month for calculation.

- Target Net Assets: Net assets targeted for the selected month of calculation.

- Diff. : Actual Net Assets – Target Net Assets.

- Analysis of Asset Achievement Rate Factors: If actual net assets cannot reach target net assets, it could be due to several reasons such as insufficient income, excessive spending, and inadequate return on investment. The analysis will be based on these three aspects to understand the reasons for not achieving planned net assets, providing a basis for modification.

- Income: Actual(Current) income accumulates to the amount as of the selected calculation month based on the set return, and it is compared with target income.

- Spending: Actual(Current) spending accumulate to the amount as of the selected calculation month based on the set return, and they are compared with target expenses.

- Net Transfer In: During the period, the amount transferred into the included account accumulates to the amount as of the selected calculation month based on the set return.

- Accumulated Return: Actual(Current) Time-weighted return rate calculates the actual investment cumulative return. Target is calculated based on the set annual return, representing the accumulated return expected during the period.

Asset Comp. Chart

Coverage Analysis

- Following the prioritized and designated family responsibilities, financial goals are listed sequentially, with the current monthly budget automatically set as the top priority.

- Family Responsibility: The total present value of financial goals is classified as family responsibilities.

- Current Coverage: Please refer to the Current Coverage

- Need Coverage: Family Responsibility – Current Coverage

- Listed Need Coverage: The present value of the financial goal calculated based on the ann. return.

- Coverage%o: The proportion of existing coverage deducted from the listed coverage needs, expressed as a percentage of the listed coverage needs.

Current Coverage

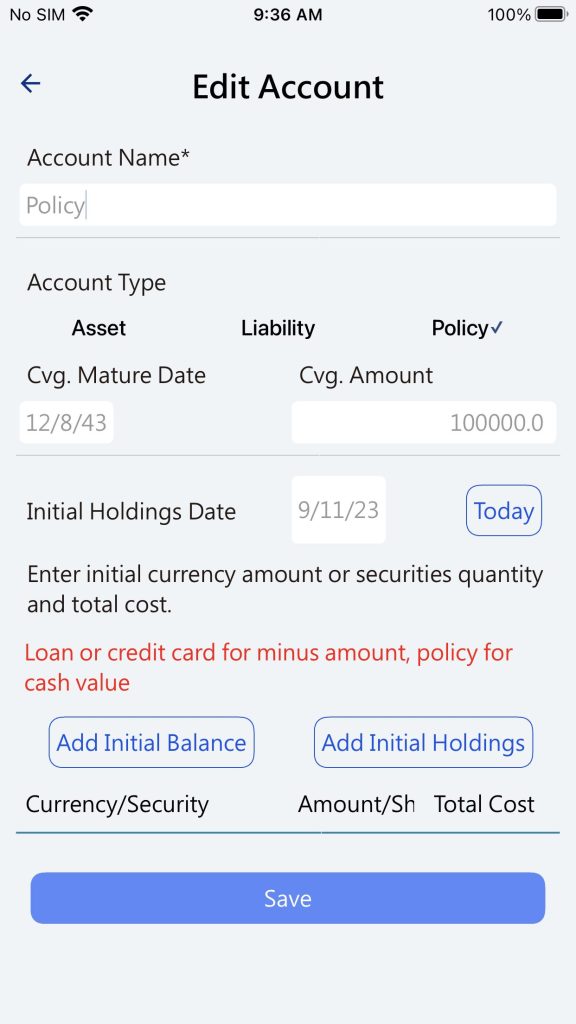

Vision Money treats insurance policies as accounts. To add a policy, go to the main function page -> Accounts -> Click on Add Account(+), choose “Policy” as the account type. Enter the life insurance coverage and the expiration date of the coverage. If it’s a lifetime coverage, you can input the expiry date. You can choose the cash value of the policy in currency and select the investment securities. This will be included in the total asset value.

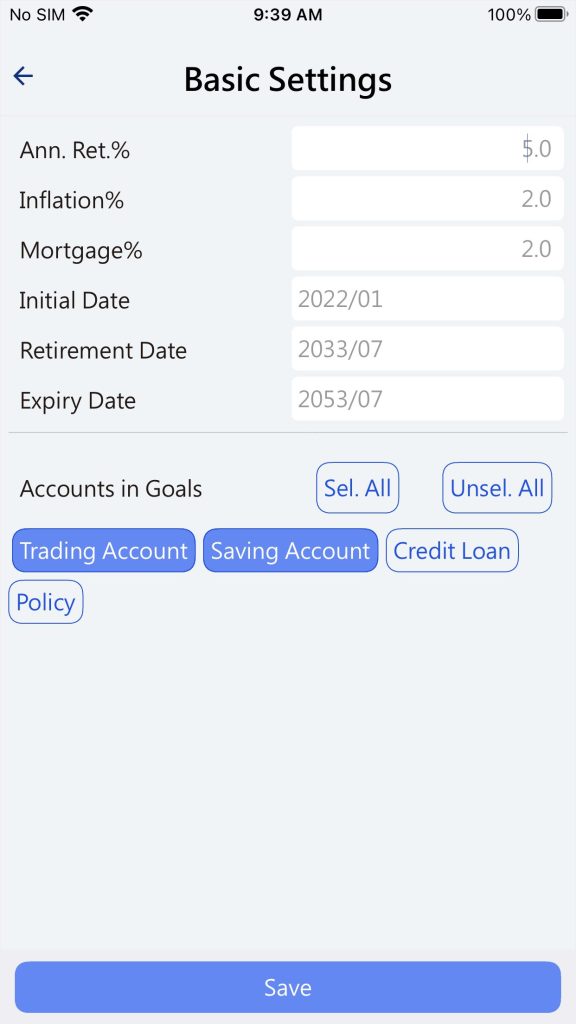

Basic Settings

Click Option(Gear)->Basic Settings

- Initial Date: As of this month, the initial asset balance for the goals is based on the value of the assets included in the included accounts as of this month. It also serves as the start date for budget goals.

- Retire Date: The default end month for budget income and expenses can be modified individually in the budget goal settings.

- Expiry Date: This is the individual’s life termination date. All asset balances are calculated up to this date.

- Accounts in Goals(Included Accounts): Select the existing accounts to calculate asset balances, actual income and expense amounts for each period.

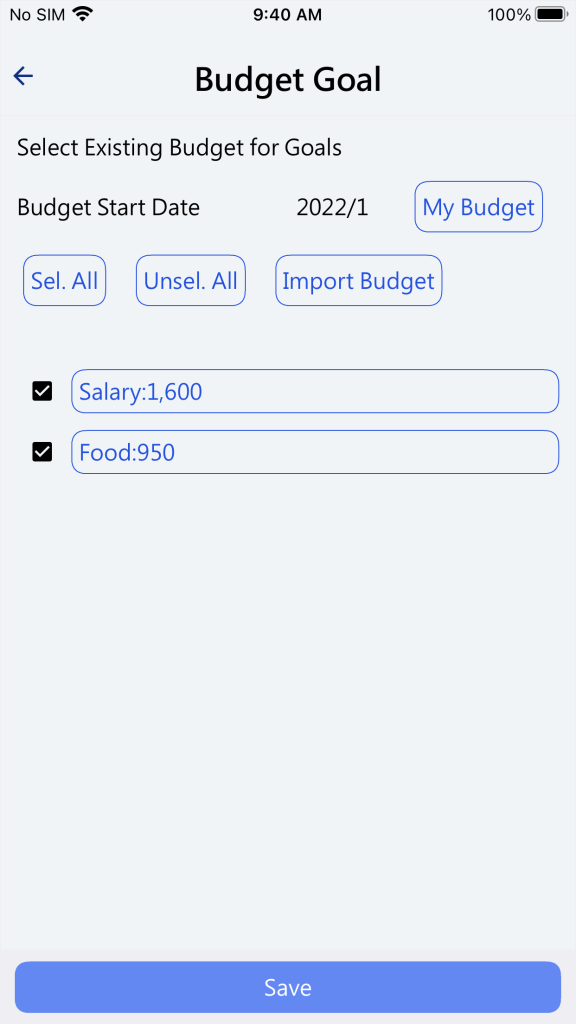

Budget Goals

Click Option(Gear)->Budget Goals

Incorporate the budget as a goal, with the budget taking precedence as the top priority, surpassing all financial goals. The default end date is set as the retirement month. The start month for the plan budget is uniformly set to the initial date.

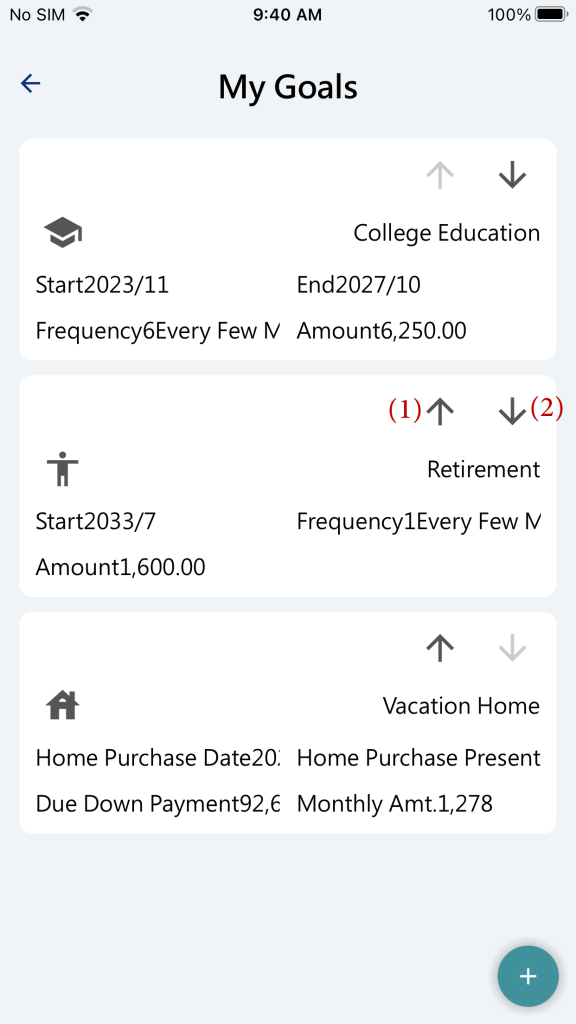

Goals Settings

Click Option(Gear)->Goal

Financial goals are categorized into College Education, retirement, home purchase, other income, other spending, etc. You can modify the names of goals as needed.

Click the upward arrow(1) to increase the priority of this goal, and click the downward arrow(2) to decrease the priority of this goal.

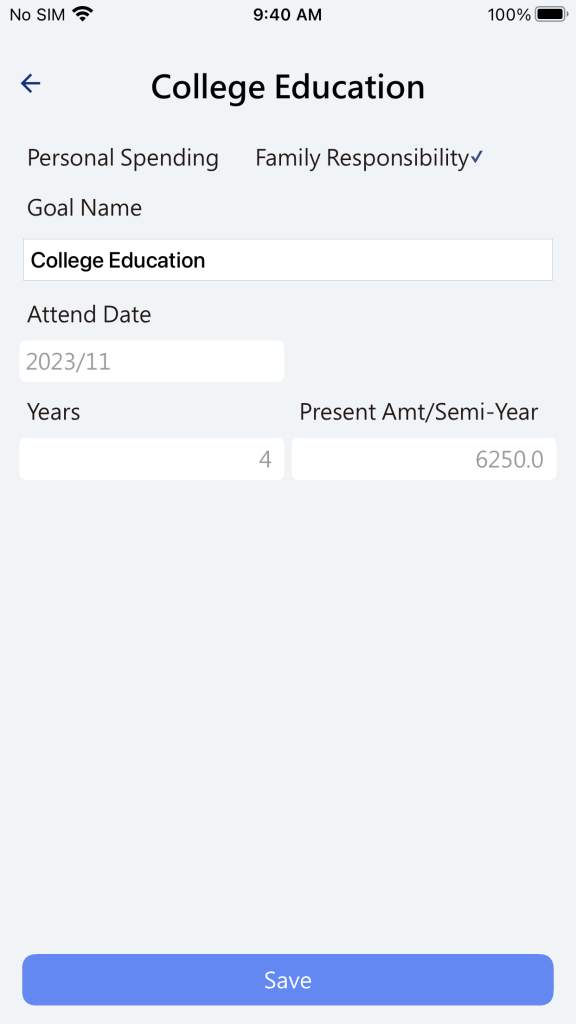

College Education

Click on the + green circle button, and choose College Education.

- Personal Spending/Family Responsibility: If you choose family responsibility for this goal, it will be included in the calculation of family responsibility coverage.

- Years: Number of years for College Education.

- Present Amount/Semi-Years: Amount as of the initial date, which will automatically adjust based on the inflation rate in subsequent periods.

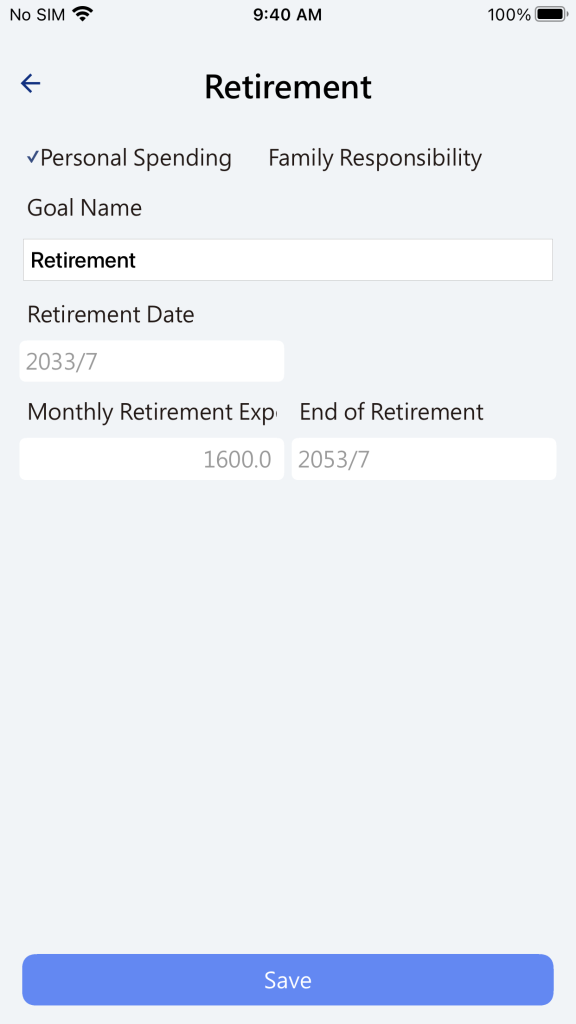

Retirement

Click on the + green circle button, and choose Retirement.

- Personal Spending/Family Responsibility: If you choose family responsibility for this goal, it will be included in the calculation of family responsibility coverage.

- Monthly Retirement Expense: The present value as of the initial date, which will automatically adjust based on the inflation rate in subsequent periods.

- End of retirement: Default is set to the Expiry Date.

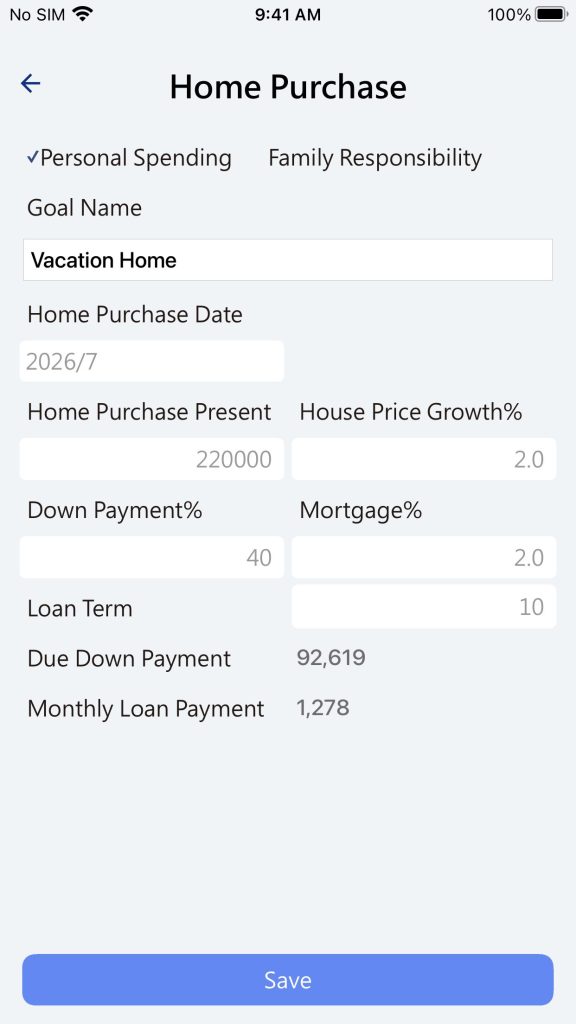

Home Purchase

Click on the + green circle button, and choose Home Purchase.

- Personal Spending/Family Responsibility: If you choose family responsibility for this goal, it will be included in the calculation of family responsibility coverage. If the home purchase is for leisure or vacation purposes in retirement, it is considered personal consumption. If it is for family residence, then it is considered a family responsibility.

- Home Purchase Present Value: The present value as of the initial date, which will automatically adjust based on the House Price Growth% in subsequent periods.

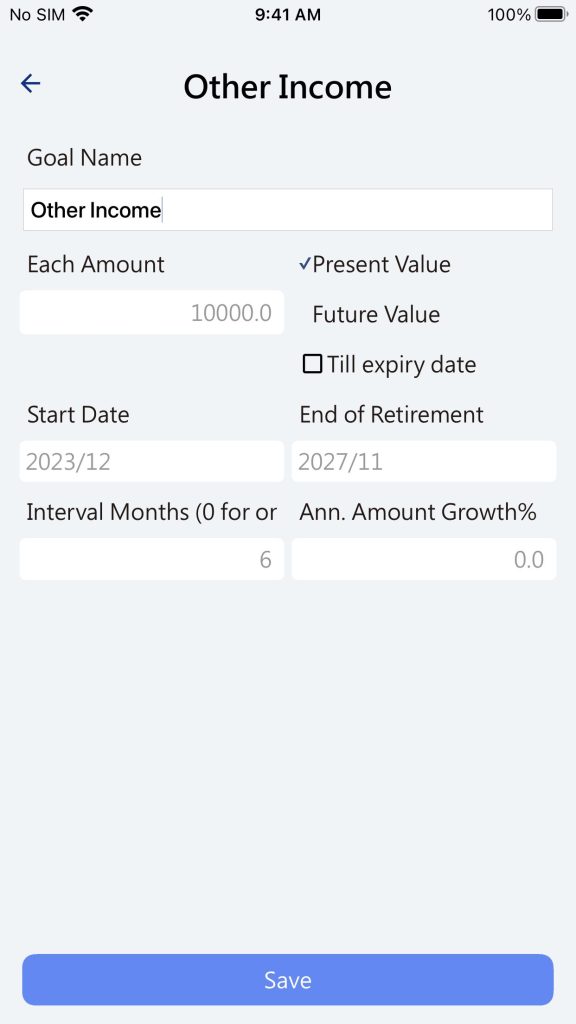

Other Income

Click on the + green circle button, and choose Income.

- Present Value: Each Amount is the present value at the initial date, which will be automatically adjusted annually based on the Ann. Amount Growth% of increase.

- Future Value: Each Amount is the value at the initial date, subsequently automatically adjusted annually based on the Ann. Amount Growth% of increase.

- Interval Months(0 for 1-time): Interval months for each occurrence of this income, with 0 indicating a one-time event.

- End of Date: End date of income.

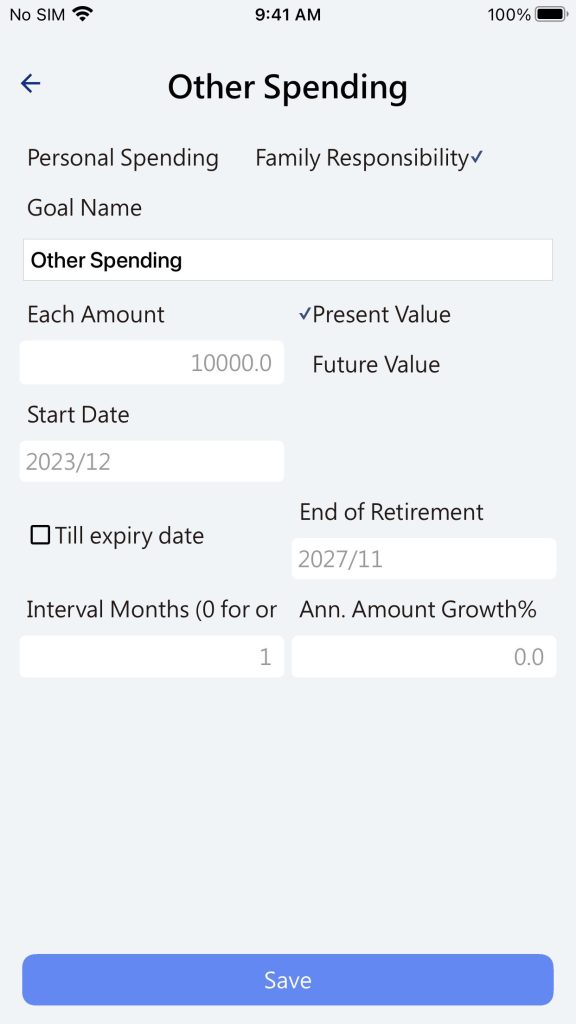

Other Spending

Click on the + green circle button, and choose Spending.

- Personal spending/family responsibilities: If this goal is selected as family responsibility, it will be included in the calculation of the family responsibility coverage amount.

- Present Value: Each Amount is the present value at the initial date, which will be automatically adjusted annually based on the Ann. Amount Growth% of increase.

- Future Value: Each Amount is the value at the initial date, subsequently automatically adjusted annually based on the Ann. Amount Growth% of increase.

- Interval Months(0 for 1-time): Interval months for each occurrence of this income, with 0 indicating a one-time event.

- End of Date: End date of spending

Dashboard displays the status of goal achievement.