1. You Don’t Need Daily Expense Tracking Anymore

If you’re reading this, your financial situation is probably very different from the “chaotic user” that most budgeting apps are designed for.

You’re probably not someone who:

- runs out of money at the end of the month

- constantly wonders where the money went

- has to control every single purchase just to stay afloat

Your situation usually looks more like this:

- Your income is stable and regular.

- Your monthly spending doesn’t change much.

- You can consistently save part of your income.

- Your spending is reasonable, without wild swings.

On the surface, everything looks stable.

But what really worries you is not “how much you spent today.”

What really worries you is:

- Are we saving fast enough to support retirement?

- Will our children’s future education cost far more than we expect?

- Is our investment performance truly “enough,” or just “not losing money”?

- If we keep going at this pace, where will we be 20 years from now?

The essence of these questions is:

Instead of tracking every small detail (budgeting),

it’s more important to manage your overall financial trajectory.

Daily expense tracking, spending categories, and pretty pie charts

cannot answer whether your retirement, education, and long-term family finances are safe.

If your income and lifestyle are already stable,

“budget control” is no longer the main issue.

What really matters is:

Can the path you are on now safely carry you to the future you actually want?

And Vision Money is designed specifically for this need.

2. From Budget Control to Trajectory Management: What You Really Need Is Not Budgeting

Think of your financial life as a long-distance flight:

- Budgeting is like watching your fuel consumption gauge.

- Trajectory management is making sure the plane can reach its destination without running out of fuel midair.

If your income is stable and your spending is stable, then:

- You already know your “fuel consumption” is steady.

- You already know you’re not overspending wildly.

- So staring at the fuel gauge every day (budgeting) becomes a poor use of time.

At this point, the real questions become:

- Where are your assets right now?

- How much should you have at this point in time?

- At your current pace, can you actually reach your future education/retirement goals?

- If not, where is the problem?

Most apps can only stop at:

- You spent too much on restaurants.

- Entertainment is over budget.

- Your budget is insufficient.

None of that can answer long-term financial questions.

Vision Money focuses on the level that actually matters:

Instead of looking at how much you spend every day,

it looks at whether your net worth is aligned with your life trajectory.

Its core method is:

Update balances, instead of recording every single transaction.

Through changes in balances, the system can accurately estimate:

- how much you are actually saving

- how much you gained or lost from investments

- how much moved between accounts

- whether your net worth is staying on its target trajectory

This is Balance-Based Tracking.

3. Balance-Based Tracking: The Best Fit for Stable-Income Families

The principle of Balance-Based Tracking is very simple:

You don’t need to record how much you spend every day;

you just need to regularly update the balance of each account.

From this, Vision Money automatically calculates:

- your saving capacity

- your investment return contribution

- the impact of transfers and large spending

- changes in your net worth

- whether your financial position is behind or ahead of plan

Unlike traditional budgeting, which requires heavy input, this approach is:

One balance update → a complete financial view.

Why is this especially suitable for stable-income families?

3.1 Long-Term Sustainability (You Can Do It for 10–20 Years)

Updating 10–15 balances once a month is easy.

Doing detailed daily budgeting for many years is unrealistic.

3.2 Directly Targets the Core Issues of Retirement and Education

What you need to know is not:

- Which extra meal you had yesterday.

But rather:

- Are your assets growing in line with your life goals?

- Are your investment returns sufficient to support the future?

- At your current pace, will you have a shortfall at age 70?

- Will there truly be enough money when your child goes to college?

Balance-Based Tracking can answer these questions accurately.

3.3 Perfect Integration with the My Goals Engine

As long as you have:

- account balances

- investment holdings (auto-synced in Platinum)

- long-term goals set up

Vision Money can draw your financial trajectory for the next 20–40 years, and:

Compare your current assets with the assets you should have at this point in time.

You are no longer staring at monthly income-and-spending summaries,

but at a complete financial flight path.

4. Your Only Core Monthly Task: Updating Balances (Cash Accounts)

For Platinum users, investment accounts are synced automatically, so:

What you really need to update each month are the non-synced cash accounts.

Including:

- salary accounts

- joint household accounts

- savings accounts

- emergency funds

- any accounts that cannot be connected to a bank

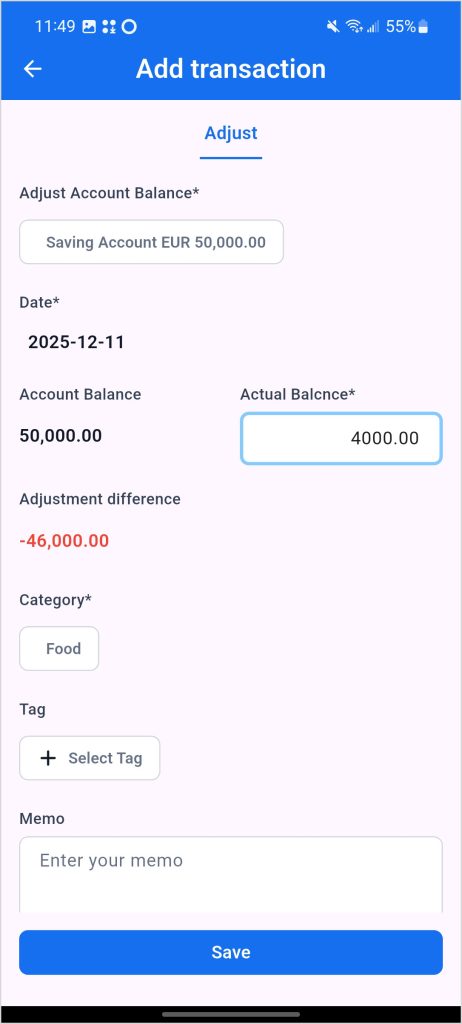

4.1 How to Adjust a Balance

- Open Accounts

- Tap the account

- Tap Adjust Balance

- Enter the actual balance

- Choose the reason for the change (Category):

- Income

- Spending (only large or unusual spending needs to be recorded)

- Transfer (lending money, moving funds)

- Investment (usually not needed for non-investment accounts)

- Add a note (optional)

- Save

Vision Money uses this information to:

- run Cause Analysis

- break down asset growth

- compare long-term trajectories

You don’t need to track every daily transaction—

you only need to stay on top of balance changes.

5. Investment Tracking (Platinum: Automatic Sync)

For stable-income families, investments are usually the most important variable.

Vision Money Platinum will:

- automatically sync your holdings

- automatically update market values

- automatically download trade history

- calculate time-weighted rate of return (TWR)

- compare your returns to the target return defined in your plan

You do not need to manually update investment balances.

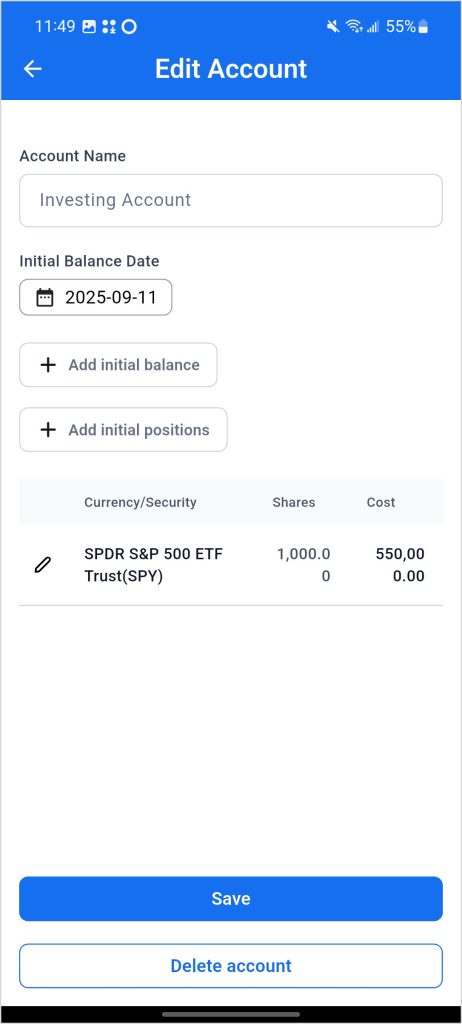

5.1 Initial Position (One Time)

If you already have holdings when you start:

- you can enter Initial Positions, and

- use automatic sync to import prices

After that, everything is automatic.

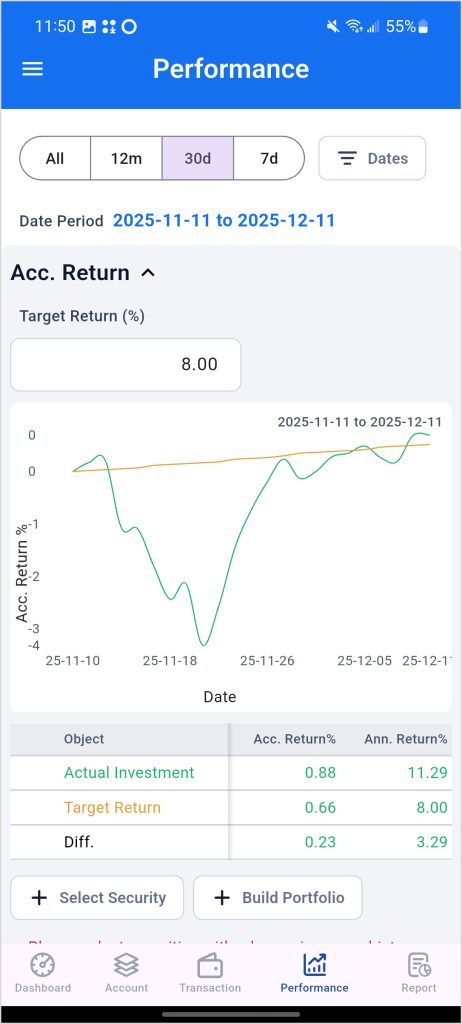

5.2 Performance: Your Most Important Investment Dashboard

The Performance page shows:

- a true, comparable investment return (TWR)

- whether it is sufficient relative to your target return

- where returns come from (by security, account, period)

Your focus is not:

“Did I make money this year?”

But:

“Is this return sufficient to support my retirement and education goals?”

6. My Goals: Building Your Overall Life Financial Trajectory

My Goals is the core engine of Vision Money.

It combines:

- starting assets

- monthly/annual net income

- goals (retirement/education)

- investment assumptions

- inflation

to generate a complete life financial trajectory.

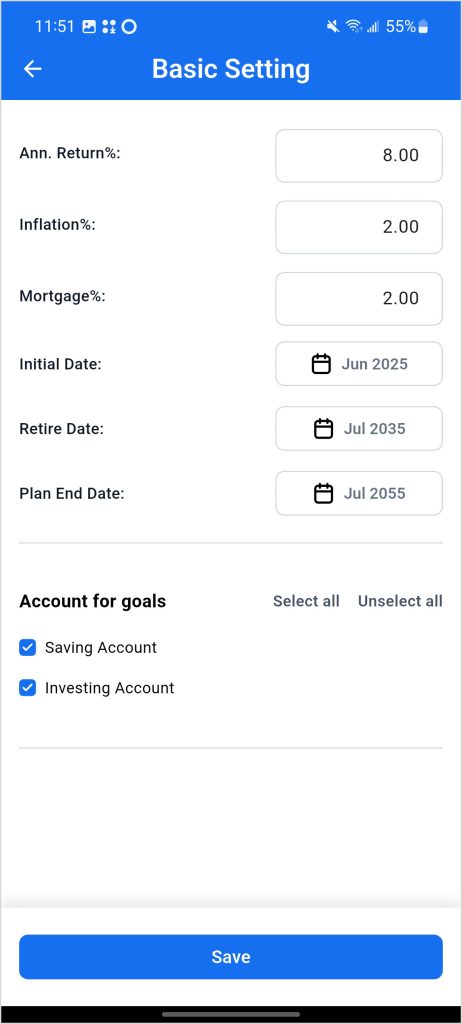

6.1 Basic Settings: Choose Accounts Included in the Plan → Automatically Create Starting Assets

In Basic Settings, you will set:

- long-term return

- inflation

- retirement age and end-of-plan age

Most importantly:

Choose which accounts to “Include in Plan.”

Vision Money will:

- sum the balances of these accounts → treat this as your starting assets

- base all future trajectory and checks on this number

This reflects Vision Money’s planning logic:

The plan looks at your total asset pool, not scattered small accounts.

6.2 In a Stable-Income Scenario, You Don’t Need Budget Control

For the target audience of this article (Stable Income Families):

- income is predictable

- spending is stable

- you don’t need to control every spending category

Therefore:

You do not need to use My Budget to restrict or track monthly spending.

The focus of the plan lies in the next step: Net Income.

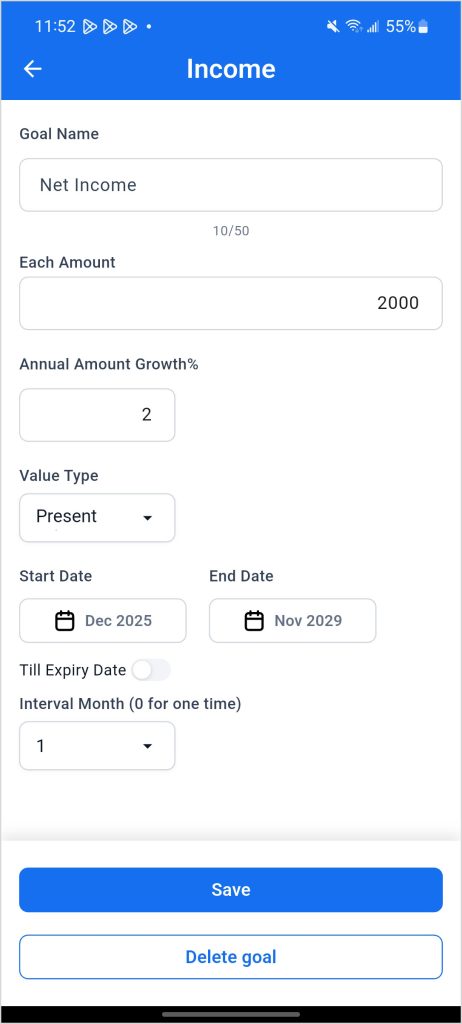

6.3 Enter Your Monthly or Annual Net Income: The Engine of the Plan

In the Stable Income mode, you only need to answer:

How much can you consistently save each month or each year? (Net Income)

Vision Money will treat net income as:

- new assets added each year,

- automatically incorporated into your long-term trajectory.

You do not need to break down spending.

Small daily spending does not need to be recorded—the balances will naturally reflect it.

7. Minimum Required Return: What Return Does Your Plan Need?

Minimum Required Return tells you:

Under your current goals and assumptions, what minimum investment return do you need for the plan not to fail?

This number is driven by:

- starting assets

- net income

- length of the plan

- retirement/education goals

As long as you don’t change the plan, this number will not change.

If your actual return is lower than this number:

- your goals will develop a shortfall at some future point.

If your actual return is higher:

- the plan becomes safer, with more buffer.

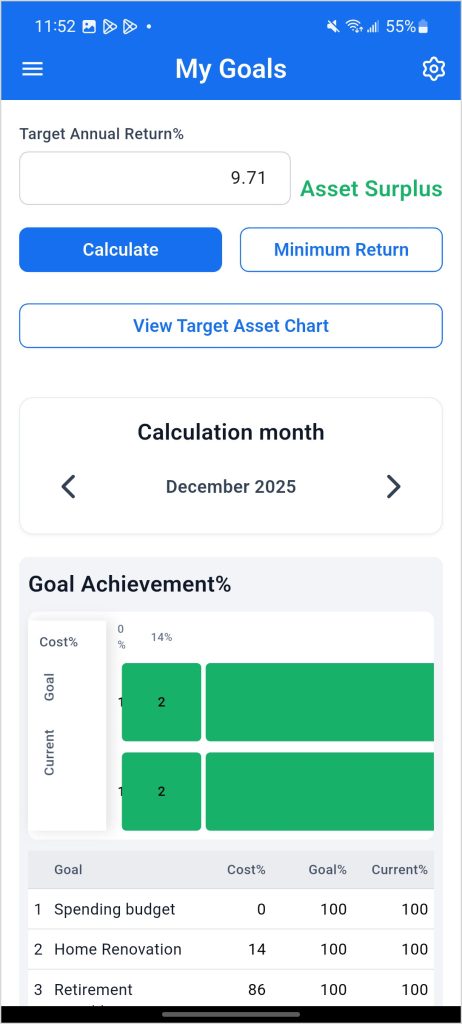

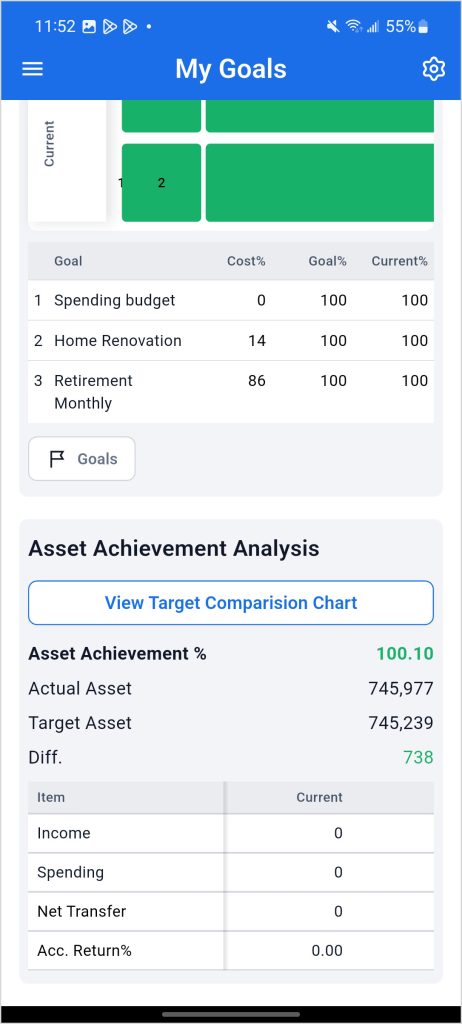

8. Asset Achievement %: Are You Ahead, On Track, or Behind?

Asset Achievement % compares:

- your actual current assets

- the assets you should have at this point in time

For example:

- You should have $500k, and you actually have $550k → 110% (ahead)

- You should have $400k, and you actually have $360k → 90% (behind)

This is the clearest statement in long-term financial management:

Are you on track right now?

9. Cause Analysis: If You’re Behind, Where Is the Problem?

Cause Analysis answers:

Why are you behind (or ahead)?

The system breaks changes into four components:

- Income

- Spending (only large events)

- Transfers

- Investment Return

You will clearly see:

- Is it insufficient income?

- Is it underperformance in investment returns?

- Is it the impact of major spending?

- Is it too much money moved out of your asset pool?

You don’t need to guess—the system reveals the real drivers.

10. Your Long-Term Financial Operating System

10.1 Monthly Routine (30–45 Minutes)

- Update balances (cash accounts)

- Optionally record large or unusual events

- Review investment performance (Performance)

- Check Asset Achievement % (are you still on track?)

If there are no major changes → you’re done.

10.2 Every 3–6 Months: Review the Plan Itself

You’re not reviewing returns—you’re reviewing the plan:

- Has your income changed?

- Has your lifestyle level changed?

- Have you added any major new goals?

Only when you modify plan assumptions

will Minimum Required Return change.

11. What Vision Money Intentionally Does Not Do

Vision Money does not:

- tell you which stocks to buy

- provide investment advice

- promise any specific rate of return

The role of Vision Money is:

To use math and trajectories to help you see your future clearly.

It is not here to lead you in picking investments,

but to let you know:

- where you are now

- where you should be

- and whether you’ll reach the destination

12. Conclusion: Stable Income Is a Superpower—As Long As You Don’t Fly with Your Eyes Closed

Stable income and stable spending are very good conditions to have.

The real risk is not reckless spending, but:

Your assets gradually drifting off course—without you noticing.

Vision Money uses:

- Balance-Based Tracking

- Investment Tracking (automatic sync)

- Minimum Required Return

- Asset Achievement %

- Cause Analysis

to give you:

A clear and dependable financial flight path.

You don’t need to track every expense every day.

You only need to know:

Is your current position aligned with where you’re supposed to be?

And Vision Money is built to give you that answer.

FAQ

Q1. Do I have to completely stop tracking expenses?

No.

You can use a “large-transaction only” approach:

- large spending

- lending money

- major transfers

Just use Adjust Balance to record them.

Everyday small spending will be naturally reflected through balance changes.

Q2. How many accounts should I track?

You only need to track:

- salary accounts

- savings accounts

- investment accounts (auto-synced in Platinum)

- retirement accounts

- other important assets

You don’t need to track useless or minor accounts.

Q3. Can I still use Vision Money if my income isn’t perfectly stable?

Yes.

Balance-Based Tracking naturally absorbs fluctuations.

Q4. How often should I review my plan?

- Update balances and performance monthly.

- Review plan assumptions every quarter or every six months.

Q5. What if my Asset Achievement % is below 100%?

Check Cause Analysis to see which factor is responsible:

- lower income

- insufficient investment return

- large spending

- funds moved out of your asset pool

Q6. Does Minimum Required Return change over time?

No.

It only changes when you modify your goals or plan assumptions.

Q7. Can I add new goals?

Yes.

The system will recalculate your trajectory and Minimum Required Return.

Q8. Is Vision Money useful if I don’t invest?

You can still use it.

But for long-term financial planning, investing is practically essential.

The system will still help you understand your net worth and future needs.

Q9. What is the minimum I need to do to use Vision Money effectively?

Three things:

- Update balances monthly

- Record large events (optional, but helpful for analysis)

- Set up your plan (starting assets, net income, education and retirement goals)

These three steps are enough

to let you clearly see your financial trajectory.