Irregular income feels chaotic—but your saving plan doesn’t have to be.

Most irregular earners fail not because they lack discipline, but because they use a system that assumes:

- Income is stable

- Savings happen evenly every month

- A bad month resets everything

Vision Money uses a different approach:

Direction over willpower.

Trajectory over monthly guessing.

Progress over income noise.

This guide shows exactly how to set up Vision Money to create a saving plan that works even when your income jumps around—using:

- A stable spending baseline

- A yearly Income Goal (Cash-In)

- A multi-year Saving Goal (Cash-Out)

- A mathematical required path

- AAR + Cause Analysis to keep you aligned

Let’s build your system step by step.

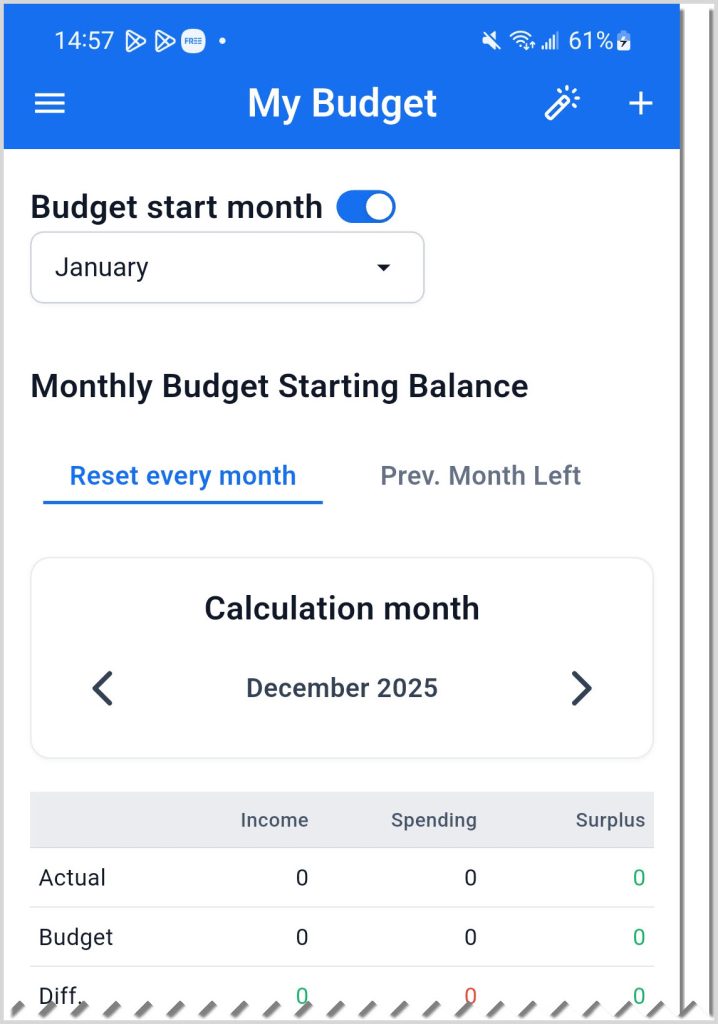

Step 1 — Build Your Spending Budget (My Budget)

(Budget = spending only, no income input here)

Irregular income is unpredictable.

Your spending must be predictable.

Your saving pace still comes from:

Saving Pace = Income − Spending

Since income fluctuates wildly, the only way to stabilize your saving pace is to stabilize spending.

✔ How to set your Spending Budget

Menu → My Budget

- Tap Budget start month

- Set your starting month

- Choose reset rule:

- Reset Every Month

- Previous Month Leftover

- Tap +

- Add each spending item:

- Category: Food, Rent, Transport, Insurance…

- Frequency: Monthly / Every few months / Yearly

- Amount

- Tap Save

✔ Why it matters for irregular income

- Spending is the only part of the formula you fully control

- Prevents lifestyle creep during good months

- Protects your saving pace during slow months

Your income can be chaotic—your spending cannot.

This step builds your financial stability floor.

Step 2 — Record Actual Income & Spending (Your Real Data)

Irregular income cannot be estimated month by month.

Vision Money works by tracking your actual behavior, not your guesses.

✔ How to record transactions

- Tap Transaction +

- Select Income

- Select the account (the account determines the account currency)

- Enter the amount

- Choose the category (Income or Expense)

- Tap Save

For irregular income:

Enter every real income event, including:

- commissions

- freelance jobs

- gig work

- bonuses

- inconsistent pay periods

Do not smooth it.

Do not “average it.”

Let the system see the real volatility.

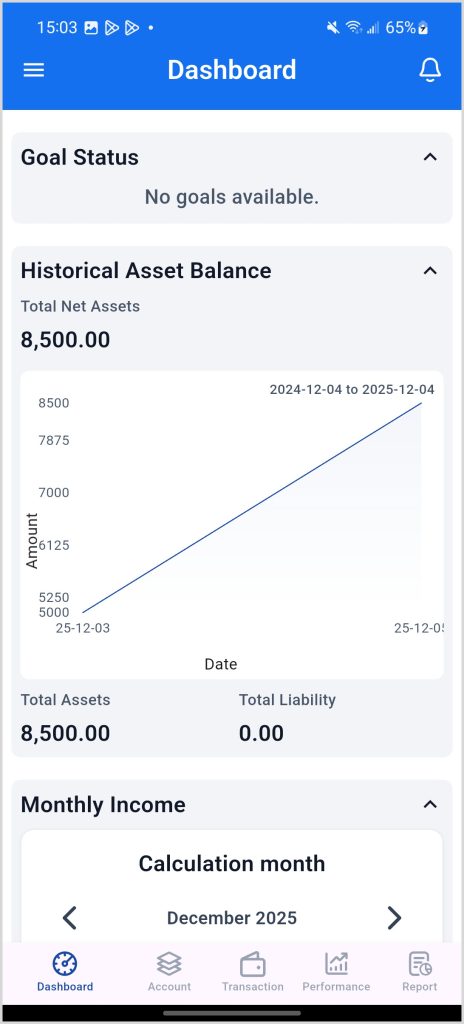

✔ Monthly review

- Dashboard → Asset Balance

Track long-term direction, not month-to-month noise - Dashboard → Budget Overspending Alerts

Immediately identifies categories hurting your saving pace

The more accurate your entries, the more accurate Vision Money becomes.

Step 3 — Set Your Annual Income Goal (Cash-In Goal)

(Your minimum realistic income baseline for the next 12 months)

This is where irregular income is handled correctly.

You cannot predict income monthly.

But you can define the minimum total income you expect each year.

This gives Vision Money the baseline for calculating your saving pace.

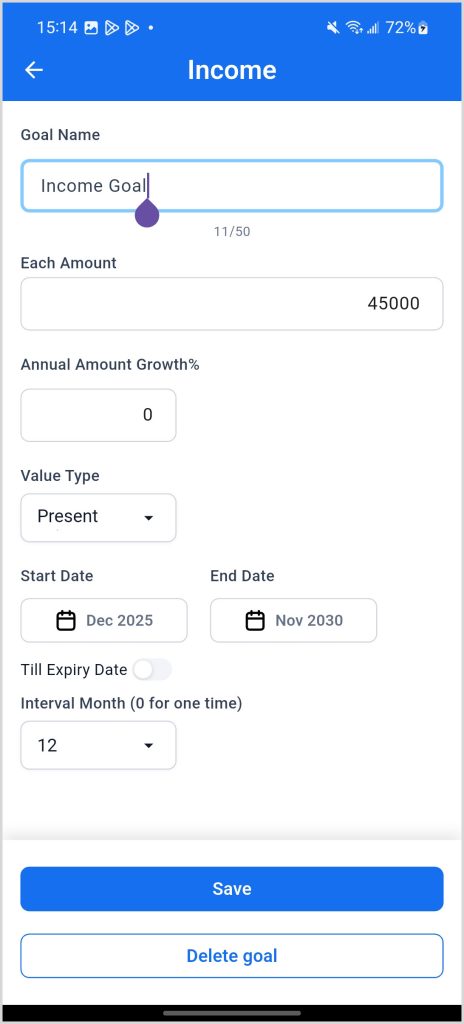

✔ How to create an Annual Income Goal

Menu → My Goals

Tap the Gear Icon → My Goals + Add Goal → Income Goal

This goal defines how much income you want to bring in during this period.

It establishes your earning baseline—even if your income arrives irregularly.

Enter:

- Goal Type: Income Goal (Cash-In)

- Amount: e.g., $45,000 per year

- Start Date: When this income period begins

- End Date: When this income period ends

- Interval Month: How often the income is expected to occur

- Set 12 months for a yearly cycle

- Set any interval that matches your pattern

- Set to 0 if this is a one-time income goal

This flexibility lets irregular earners model their income realistically instead of forcing a fixed monthly assumption.

✔ Why Cash-In Goal is essential for irregular income

- Gives Vision Money a realistic earning baseline

- Allows Target Assets to be calculated correctly

- Prevents the system from assuming “zero income months”

- Smooths out irregular earning patterns over the chosen time period

- Allows full flexibility — you can set one-time income, quarterly income, or any interval that matches your real earning pattern

This goal establishes your income trajectory for the period you define.

✔ Example for irregular income

Include (Cash-In):

- main salary

- recurring freelance income

- predictable client work

Exclude (Cash-In):

- unpredictable windfalls

- one-time bonuses you don’t want to rely on

Spending:

- include only categories relevant to saving pace

- usually exclude discretionary categories

Budget Goals = your saving engine.

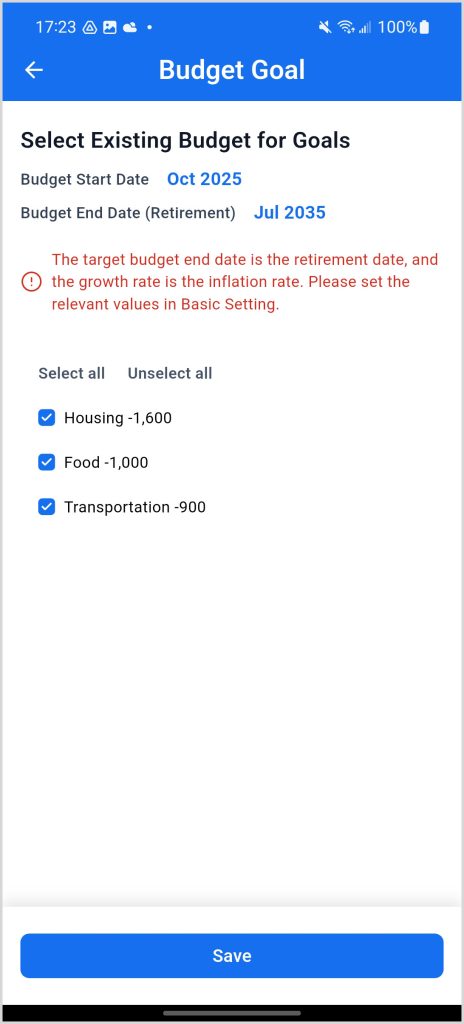

Step 4 — Budget Goals: Select Which Income & Spending Drive Your Saving Pace

Budget Goals tell Vision Money:

“Which income streams & which spending categories matter to this plan?”

This step connects your real-world finances to your Saving Goal.

✔ How to configure Budget Goals

Menu → My Goals

Tap the Gear Icon → Budget Goals

- Vision Money displays all income and spending budget items

- Select which budget items you want to include in this plan

- Tap Save

✔ Basic Setting (required foundation)

Menu → My Goals

Tap the Gear Icon → Basic Setting

Configure:

- Initial Date: This month

- Plan End Date:

- The final date used for all calculations

- The day on which the system stops projecting your saving path, return requirement, and AAR

- Ann. Return %: 0–3% recommended

- Inflation %: optional

- Included Accounts: which accounts count toward Target Assets

This defines the mathematical structure of your saving plan.

Step 5 — Add Your Multi-Year Saving Goal (Cash-Out Goal)

(Example: Save $50,000 in 5 years)

This is completely different from Step 3.

- Step 3 = Cash-In Goal (Annual income)

- Step 5 = Cash-Out Goal (Target assets)

Your long-term vision starts here.

✔ How to add your Saving Goal (Cash-Out)

Menu → My Goals

Tap the Gear Icon → + Add Goal → Spending Goal

(Saving Goal = Cash-Out. This is the goal for how much you want to accumulate.)

Enter:

- Goal Name: Saving Goal

- Goal Amount: $50,000

- Start Date: When this saving period begins

- Target Date: 5 years from now

- Value Type: Present Value / Future Value

- Interval Month: Set the saving frequency (or 0 for one-time)

Tap Save.

Step 6 — Minimum Required Return

(Your required investment return for the plan to succeed)

MWRR tells you:

“Given your saving pace and timeline, what minimum annual return must you earn?”

✔ Interpretation

- 0–4% → very realistic

- 6–8% → possible but sensitive

- 10–12%+ → unrealistic unless saving pace improves

Minimum Required Return prevents you from chasing an impossible goal for years without knowing it.

Step 7 — Target Asset Chart (Your Required Path)

(The most important tool for irregular earners)

Monthly income jumps.

Your required path must not.

✔ How to view it

Tap View Target Asset Chart.

(Screenshot: Target Asset Chart)

This chart shows exactly:

- where you should be today

- next month

- six months from now

- three years later

- final target point

It is calculated entirely from:

- your Budget Goals

- your Cash-In target

- your Spending Budget

- your expected return

If Target Assets go negative

(e.g., –$200, –$900…)

It means:

Your current saving pace cannot mathematically reach the goal.

Fixes:

- extend timeline

- improve saving pace

- reduce goal amount

Negative Target Assets are Vision Money’s strongest warning.

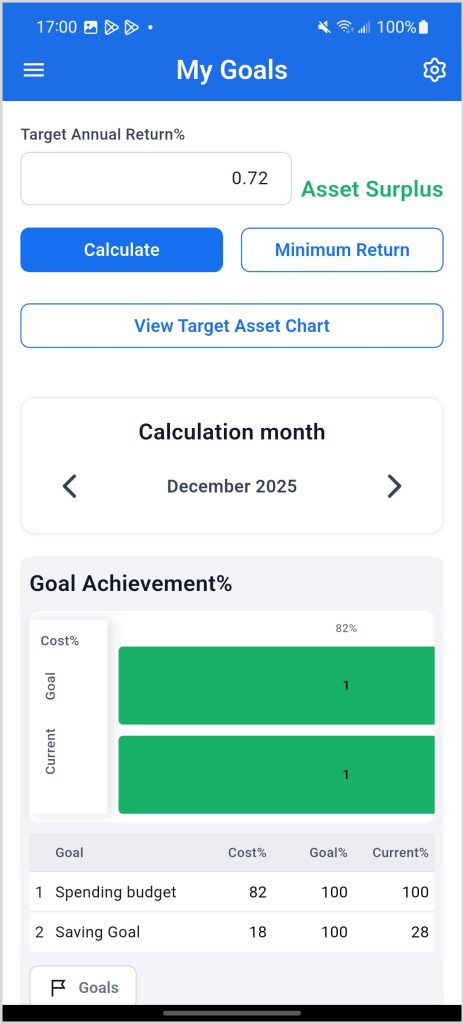

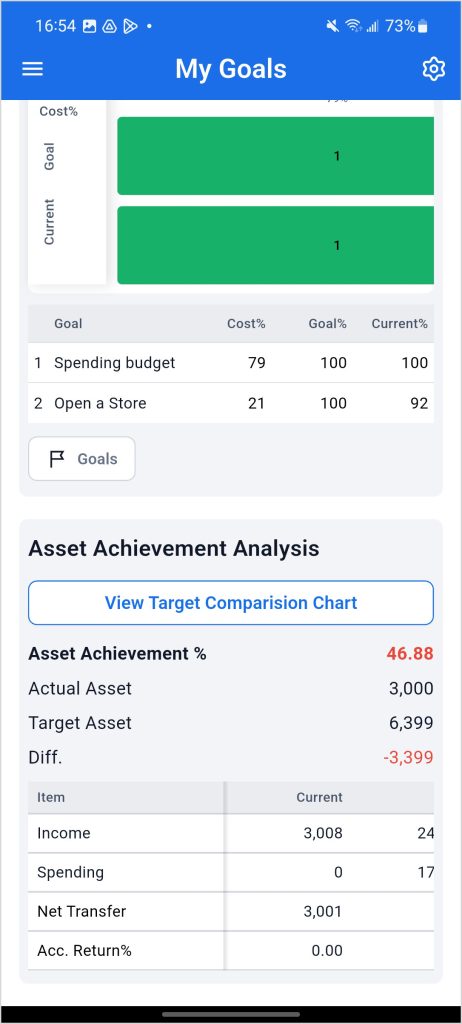

Step 8 — AAR (Asset Achievement Rate) + Cause Analysis

AAR tells you exactly:

“Am I on track today?”

No emotion.

No guessing.

Just math.

✔ Interpretation

- AAR ≥ 100% → On track

- 95–99% → Slightly behind

- < 100% → Off track

(Screenshot: AAR display)

✔ Cause Analysis reveals the reason

① Income Shortfall

Your real income was lower than your Budget Goal expectation.

Common with irregular earners.

② Overspending

Your expenses exceeded the spending baseline.

③ Accumulated Return Below Expectation

Your investments underperformed your expected return.

④ Unexpected Net Transfer

Money moved out of included accounts unexpectedly.

AAR tells you whether you’re off track.

Cause Analysis tells you why.

Step 9 — Five Minutes per Month to Stay Aligned

Irregular income doesn’t require micromanagement.

Just consistency.

Each month:

- Dashboard → Budget Overspending Alerts

- Dashboard → Asset Balance

- Check AAR

- Adjust if needed

Fixes that work best:

- reduce one flexible spending category

- allocate part of a good month to savings

- adjust timeline

- refine Budget Goals

Five minutes prevents losing five years of progress.

Conclusion

Irregular income doesn’t make saving impossible.

It just requires the right structure.

Vision Money gives you:

- A clear spending baseline

- A yearly income trajectory

- A multi-year saving direction

- A required mathematical path

- AAR that tells you the truth

- Cause Analysis so you know exactly what to fix

Your income may be irregular—but your progress won’t be.

With Vision Money, you’re not guessing.

You’re building a plan that works because it was built for volatility.