This article is for people who are already managing debt repayment.

It focuses on checking whether a repayment plan is feasible over time — not on motivation or spending tips.

Scenario: Kicking Off a Repayment Plan in Jan 2025

- Income: $3,900/month

- Essential Expenses: $2,800/month

- Rent: $1,200

- Utilities & Transport: $800

- Living: $800

- Monthly Surplus: $1,100 (all to debt repayment)

Two debts:

- Student Loan: –$48,000, 2% APR (large, long-term)

- Credit Card: –$20,000, 15% APR (high interest, minimum payment trap)

Emily thought:

“If I throw all $1,100 each month into debt, I should finish on time, right?”

Let’s run it through Vision Money and see what actually happens.

Quick Overview of the Process

- Set up liability accounts for loans (record only, don’t include in the plan).

- Basic Settings – define the timeline and assumptions.

- Budget Goals – plug income/expenses directly into the plan.

- Create repayment goals (student loan: even installments; credit card: minimum → installments).

- Assign a conservative return rate (use deposit/savings rates, ~1–2%).

- Check feasibility with the Asset Achievement %.

- Add bonus events (e.g., Sept 2025 performance bonus) and re-test.

- Track progress visually with charts.

Step 1 | Record Debt Accounts (but Don’t Add to the Plan)

Menu: Accounts → Add Account

- Student Loan: –$48,000, 2% APR

- Credit Card: –$20,000, 15% APR

See more → User Guide: Accounts/

⚠️ Important: These are just for reference. Don’t check them into the repayment plan. Otherwise, the math double-counts and throws off the Asset Achievement %.

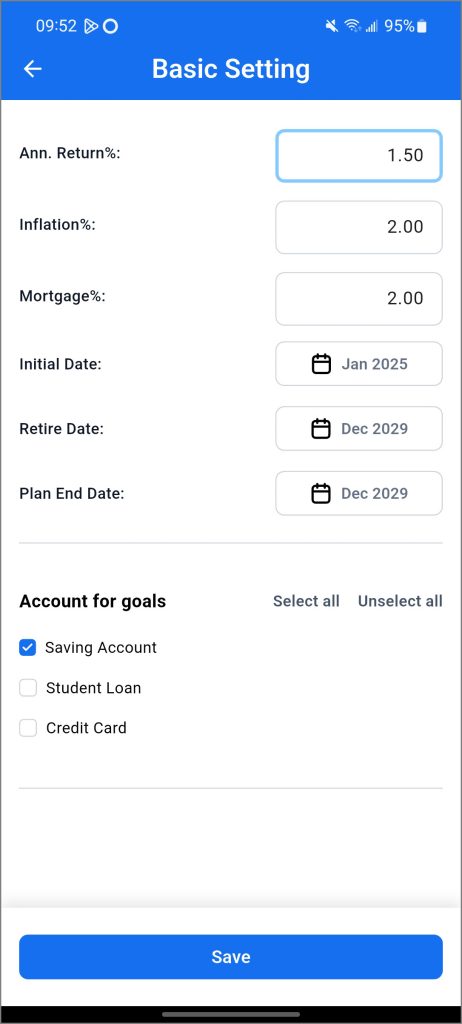

Step 2 | Set the Ground Rules in Basic Settings

Menu: My Goals → Settings → Basic Settings

- Expected return: 1.5%

- Inflation: 2%

- Start date: Jan 2025

- End date / “Retirement date”: Dec 2029 (end of plan horizon)

- Accounts included: only asset accounts

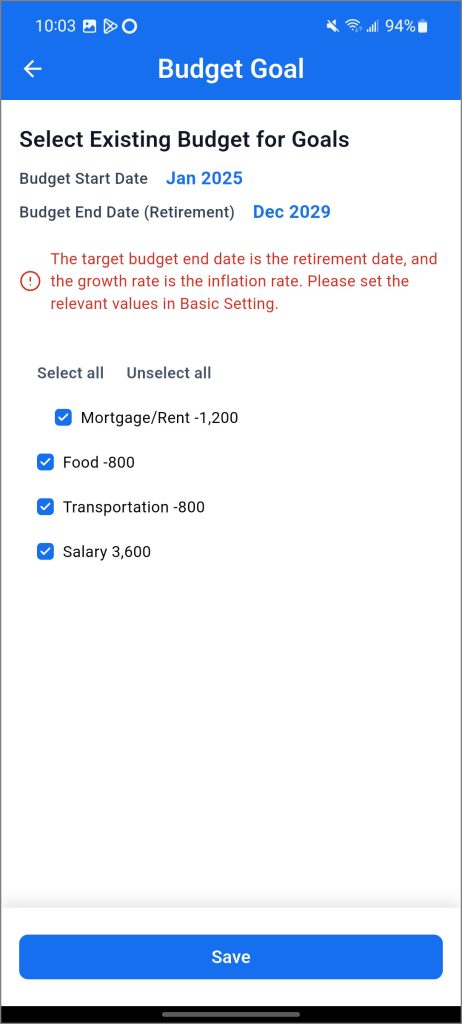

Step 3 | Connect Budget to the Plan

- Income: $3,900

- Expenses: $2,800

- Surplus: $1,100

Once you enable Budget Goals, these numbers flow into the plan automatically. No double entry.

See more → User Guide: My Budget/

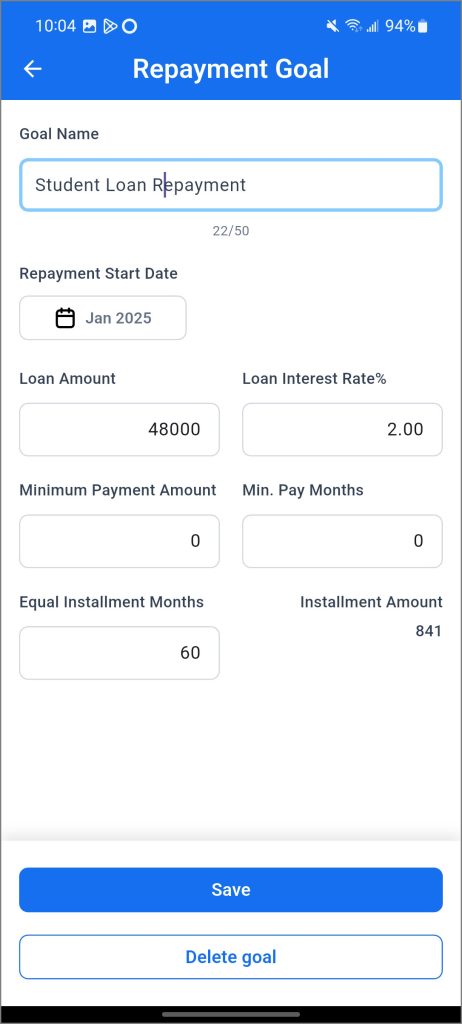

Step 4 | Build Two Repayment Goals

Student Loan

- Principal: $48,000

- Method: Regular Installments (5 years, ~$900/month)

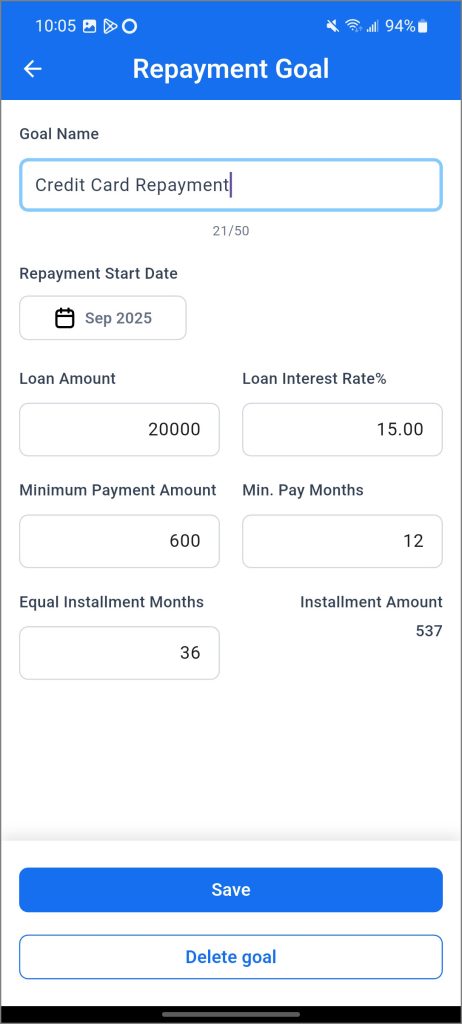

Credit Card

- Principal: $20,000

- Method:

- First 12 months → Minimum payment $100/month

- Next 36 months → Even installments

Step 5 | Conservative Return Rates

For repayment goals, set the annual return rate to 1–2% (like a savings deposit).

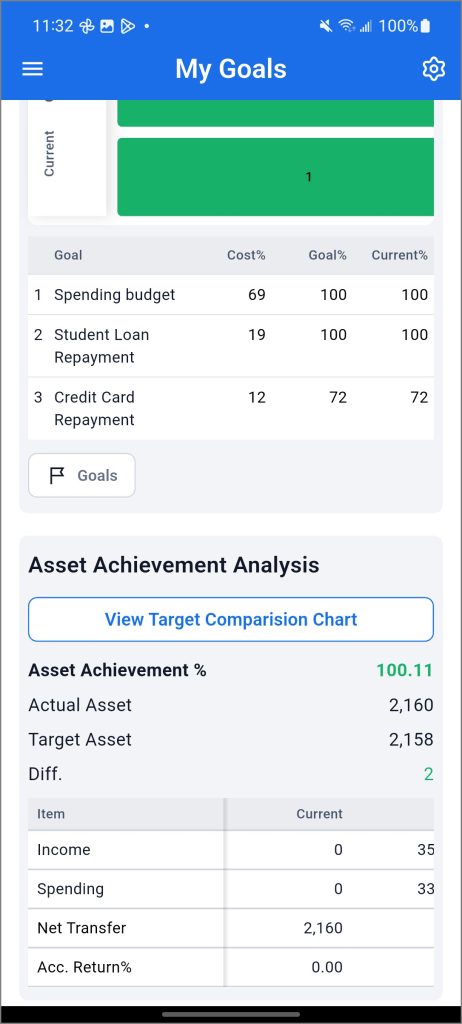

Step 6 | Check Goal Achievement

Vision Money runs the numbers:

- Budget coverage: ✅ 100%

- Student loan: ✅ 100% (achievable in 5 years)

- Credit card: ❌ only 72% (plan fails)

Emily’s reaction:

“So it’s not that I’m not trying hard. It’s that the math simply doesn’t work.”

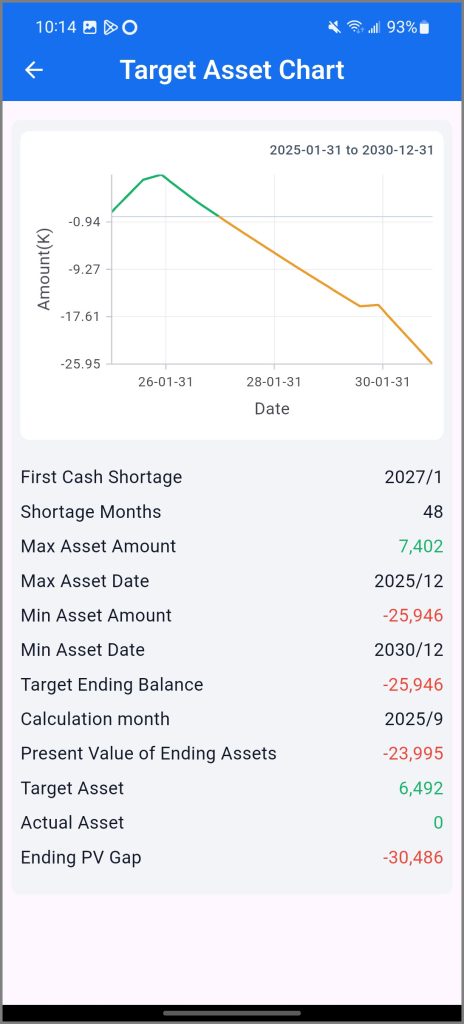

Step 7 | Track Progress with Charts

Target Asset Chart shows:

- Current assets on the left → projected balances through Dec 2029.

- Includes income, expenses, repayments, and goals.

- If feasible, the curve stays positive.

- If infeasible, the line drops into negative territory at a clear “breakdown point.”

Step 8 | Add a Bonus Event (Sept 2025)

Menu: Transaction → Income → Salary

- Add income: $8,000 → deposit to checking → apply to credit card repayment.

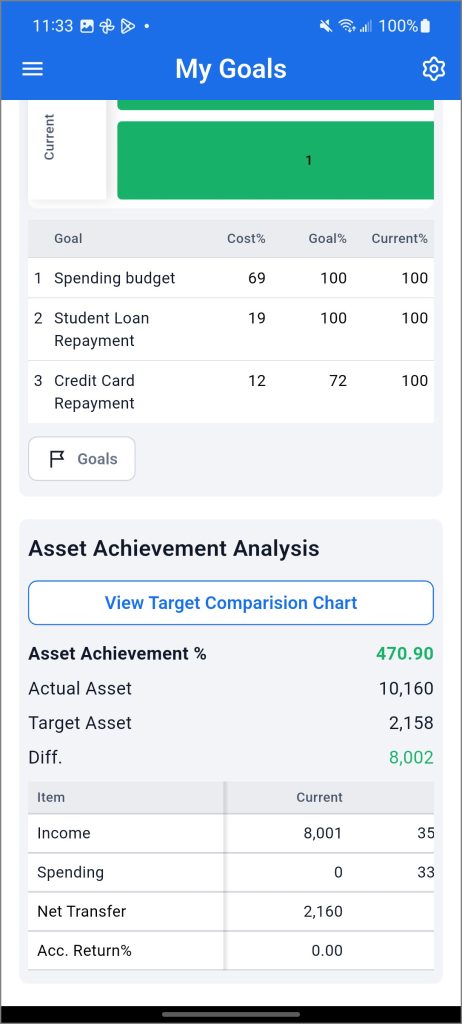

Before bonus (Aug 2025):

- Achievement: 72%

- Outcome: student loan cleared, credit card only 72%

After bonus (Sept 2025):

- Achievement: 470.9%

- Outcome: both debts fully cleared

See more → User Guide: Transaction Overview/

What-If: Buying a Used Car

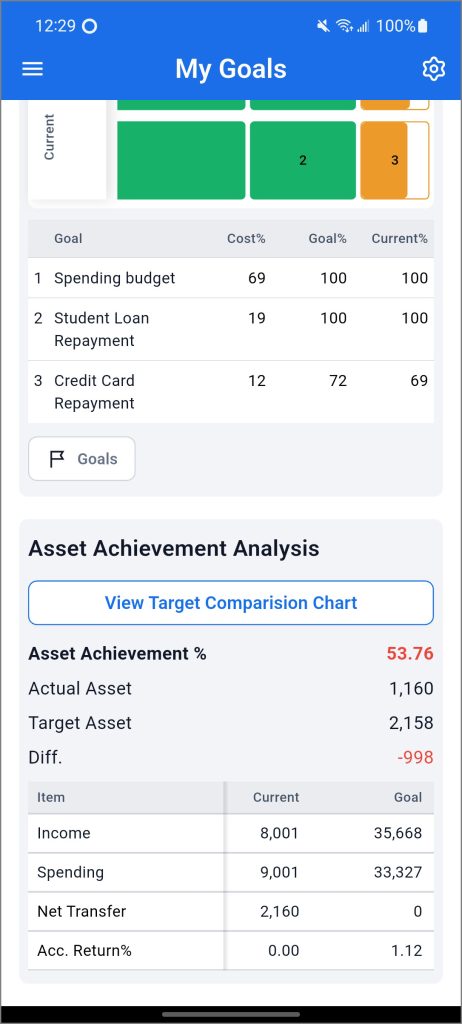

Emily wondered: “Can I buy a $9,000 used car in Sept 2025?”

She added a What-If Goal:

- Car purchase, $9,000 lump sum, Sept 2025

Result:

- Asset Achievement drops from 470.9% → 53.7%

- Credit card repayment falls to 69%

- Plan collapses again

Lesson: the car has to wait.

Why This Time It Worked

- Debt accounts recorded properly (not double-counted).

- Budget linked straight into the plan.

- Credit card modeled realistically (minimum → installments).

- Asset Achievement % exposed feasibility.

- Sept 2025 bonus flipped the plan from “impossible” to “done.”

- What-If showed clearly why buying a car now would kill the plan.

Monthly Check-In Checklist

- Verify account balances vs. planned amounts.

- Check actual Asset Achievement % vs. target.

- Confirm progress in My Goals → Asset Achievement %.

Final Word: Finishing > Trying Hard

Emily started 2025 thinking:

“As long as I pay $1,100 a month, I’ll be fine.”

Reality check: the math said only 72% feasible.

Effort alone wasn’t enough.

With Vision Money, she could actually see the gap, inject the Sept bonus, and confirm the plan was now 100% achievable.

And when tempted by that used car? A single What-If showed it would wreck her plan.

True peace of mind comes from this:

It’s not about “working harder.”

It’s about knowing you’ll finish.