If money is tight, saving can feel impossible.

Not because you’re undisciplined—but because you’re working without a system that shows:

- What pace you can realistically maintain

- How far along you should be today

- Whether you’re behind

- And why you’re behind

Most people never see these signals. They try to “save harder,” but saving harder is not the same as saving correctly. Without a structure, everything depends on willpower—and willpower collapses under financial pressure.

This article shows you exactly how to use Vision Money to build a saving system that works even when your income is limited.

With three core tools:

- A stable saving pace using your monthly budget

- A long-term Saving Goal with a mathematical required path

- AAR (Asset Achievement Rate) that tells you early if your plan is slipping

Let’s start from the foundation.

Step 1 — Build a Monthly Budget (My Budget)

When income is tight, saving always comes from one place:

Saving Pace = Income − Spending

Your monthly surplus is your saving power.

Vision Money’s budgeting system is designed to protect that surplus by preventing random, unpredictable spending spikes.

✔ How to set your budget

- Menu → My Budget

- Tap Budget Start

- Choose the starting month

- Select a mode:

- Reset Every Month — each budget category resets at month start

- Previous Month Leftover — unused budgets carry forward

- Return to My Budget

- Tap +

- Add a budget item:

- Choose category (Salary, Food, Rent, Transport…)

- Set frequency: Monthly / Every few months / Yearly

- Enter the amount

- Save

A budget does not create savings by itself—

but it protects your saving pace by giving every dollar a job.

Even $100 a month matters.

Consistent saving is built from small, stable surpluses collected over many months.

Step 2 — Record Daily Transactions

A saving plan only works if Vision Money knows your actual financial behavior.

The app calculates your saving pace based on what you really earn and spend—not what you planned.

✔ How to record transactions

- Tap Transaction +

- Select category

- Enter amount

- Save

At the end of each month, review:

- Dashboard → Asset Balance

Shows whether your total assets are trending in the right direction. - Dashboard → Budget Overspending Alerts

Lets you know immediately if a category threatens your saving pace.

The more consistent your entries, the more accurate your long-term saving trajectory becomes.

Step 3 — Set Your Saving Goal

Once your budget and spending data are ready, you can define your long-term direction.

You don’t need to calculate monthly saving targets yourself—Vision Money handles that.

You only need to decide:

“When do I want this goal completed?”

✔ Basic Setting (required foundation)

Menu → My Goals

Tap the Gear Icon → Basic Setting

Configure:

- Initial Date: This month

- Plan End Date:

- The exact date you expect the goal to be completed

- Saving Goal → the day you want the final amount

- Retirement Goal → your intended retirement date

- Ann. Return %: 0–3% recommended

- Inflation %: optional

- Included Accounts: which accounts count toward Target Assets

This defines the mathematical structure of your saving plan.

✔ Budget Goals — Select Which Budget Items Influence Your Plan

Budget Goals allows you to choose which of your budget items should be included in this plan.

This affects which income or spending categories contribute to your saving pace for the goal.

Vision Money displays:

- Income Budget Amount

- Spending Budget Amount

Tap Edit to select the budget items you want to include.

Example:

- Include: Salary, regular saving transfers

- Exclude: Food, Entertainment, Transportation

After selecting the items, tap Save.

✔ Add a Saving Goal

My Goals → + Add Goal

Select Saving Goal

Enter:

- Goal Amount (e.g., $50,000)

- Target Date (your completion date)

- Value Type (Present Value or Future Value)

- Budget Goal (which budget items fund this goal)

Tap Save.

Vision Money will instantly:

- Generate your multi-year Target Asset trajectory

- Calculate your Minimum Required Return

- Begin tracking your AAR

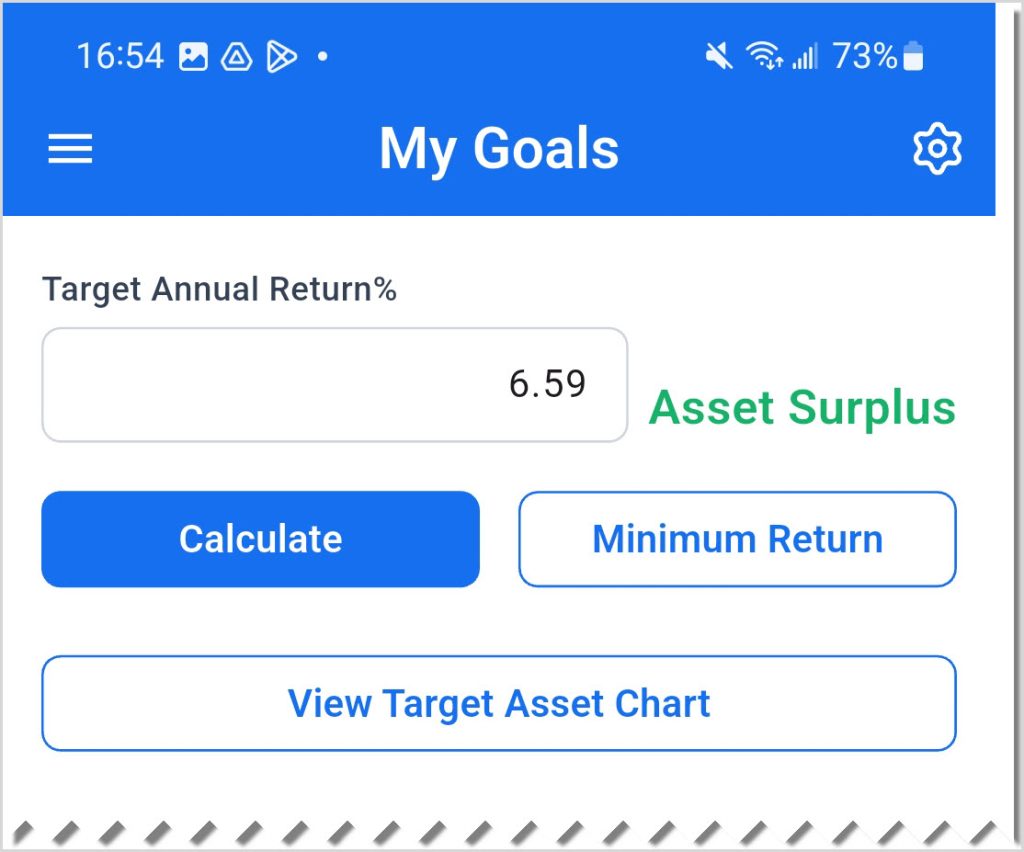

Step 4 — Minimum Required Return

This number tells you the minimum annual return needed to reach your goal based on:

- Your saving pace

- Your selected budget items

- Your target amount

- Your timeline

It’s a crucial early-warning system.

✔ How to interpret it

- 2–3% → realistic

- 6–8% → your pace may be too slow

- 10–12%+ → mathematically unrealistic

Minimum Required Return prevents painful surprises years later.

You’ll know immediately whether your plan is achievable.

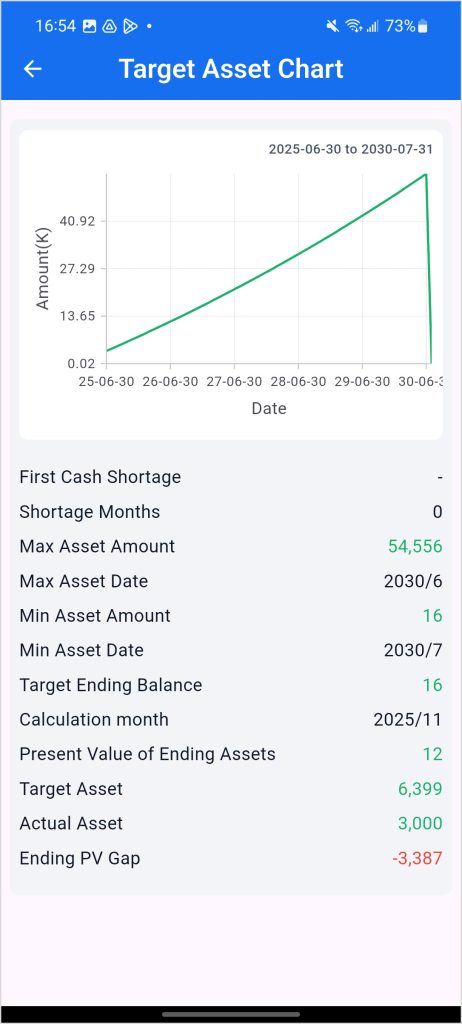

Step 5 — View Target Asset Chart (Your Required Path)

This chart answers the most important question:

“How much should I have accumulated at every point between now and my target date?”

✔ How to open it

- Tap View Target Asset Chart

You will see one single line: Target Assets.

Why only one line?

Because this line represents the required trajectory, not the actual result.

Actual numbers are used in AAR—and the chart must remain clean and focused.

The curve shows:

- Today’s required asset level

- Next month

- Six months ahead

- Three years ahead

- Your final target

It is computed from:

- Your chosen Budget Goals

- Expected return

- Timeline

- Final target amount

This line is your saving “roadmap.”

When Target Assets Become Negative

If any point on the path drops below zero:

- –$200

- –$900

- –$3,000

It means you would need to “already have negative savings” today to reach your target on time.

This is not a warning—it’s math.

The goal cannot be achieved under your current pace.

You must:

- Extend the timeline

- Lower the goal

- Increase saving pace

Negative Target Assets are Vision Money’s strongest “stop and adjust now” signal.

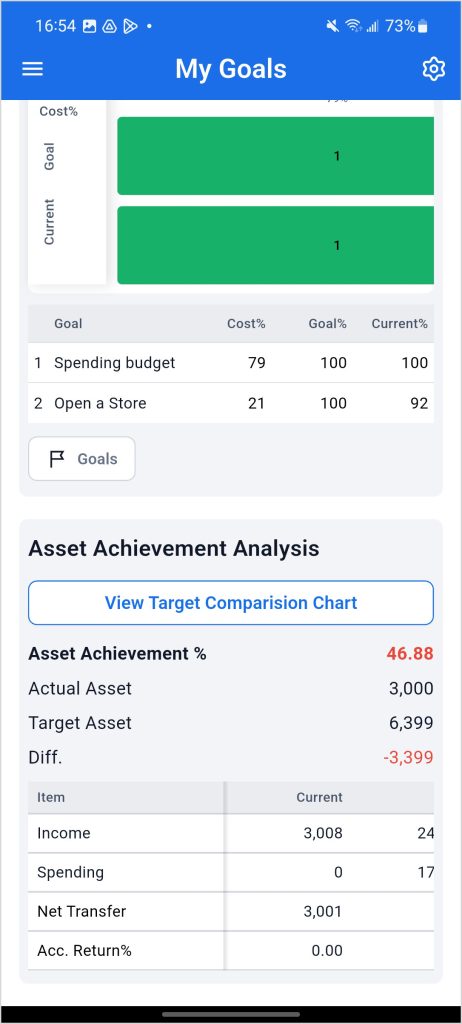

Step 6 — AAR (Asset Achievement %) + Cause Analysis

AAR tells you exactly whether you’re on track today.

Formula

AAR = Actual Assets ÷ Target Assets

✔ Interpretation

- ≥ 100% → on track or ahead

- 95–99% → slightly behind

- < 100% → off track

AAR removes emotion. It gives a clean, mathematical truth.

Cause Analysis — Why You’re Behind

Vision Money breaks the shortfall into four root causes:

① Income Shortfall

Your income was lower than planned.

Examples:

- A missed shift

- A slow freelance month

- Reduced part-time hours

② Overspending

Your expenses exceeded your saving pace.

Vision Money identifies:

- Required vs actual spending

- Overrun categories

Even small leaks add up quickly when income is tight.

③ Accumulated Return Below Expectation

Your investment performance fell short of your expected return.

Even small return gaps affect long-term trajectory.

④ Unexpected Net Transfer

Money left your included accounts unexpectedly.

Examples:

- Temporary withdrawals

- Missed saving transfers

- Shifting assets between accounts

AAR tells you whether you’re on track.

Cause Analysis tells you why.

Together, they give full visibility over your saving trajectory.

Step 7 — Core Reasons Behind an AAR Below 100%

Most issues fall into:

- Saving pace too slow

- Overspending

- Timeline too short

- High Minimum Required Return

- Negative Target Assets

Vision Money doesn’t show symptoms—it reveals causes.

Step 8 — The Three Most Effective Fixes

These adjustments create the strongest, fastest recovery:

✔ 1) Reduce one spending category

Even a small reduction creates meaningful improvement over time.

✔ 2) Add a one-time income injection

A single intentional transfer can lift your AAR above 100%.

✔ 3) Extend the target date

My Goals → Saving Goal → Edit → Target Date

Even a 3–6 month extension can dramatically stabilize your trajectory.

Step 9 — Five Minutes a Month to Stay Aligned

To prevent long-term drift:

- Dashboard → Budget Overspending Alerts

- Dashboard → Asset Balance

- Check AAR

- Adjust if necessary

It takes five minutes—

but it prevents losing five years of progress.

Conclusion

Saving consistently when money is tight is not about perfection.

It’s about having:

- A clear direction

- A realistic pace

- A quick check-in that keeps you aligned

Vision Money provides all three.

With structure instead of stress, saving becomes predictable, achievable, and motivating—even on a limited income.

With the right system, you’re not just hoping to save.

You’re actually doing it.